The ransom note flashed on every hospital screen: “Pay 87 BTC or we leak 100k patient HIV records.”

I called our cyber insurer, sweating. “We’ve got $10M coverage!” I gasped.

Their response? “Let’s review your policy exclusions first.”

Spoiler: They paid $0.

The $10M Mirage

Cyber insurance promises a safety net. Reality? It’s full of trapdoors. After auditing 37 policies, here’s what you actually get.

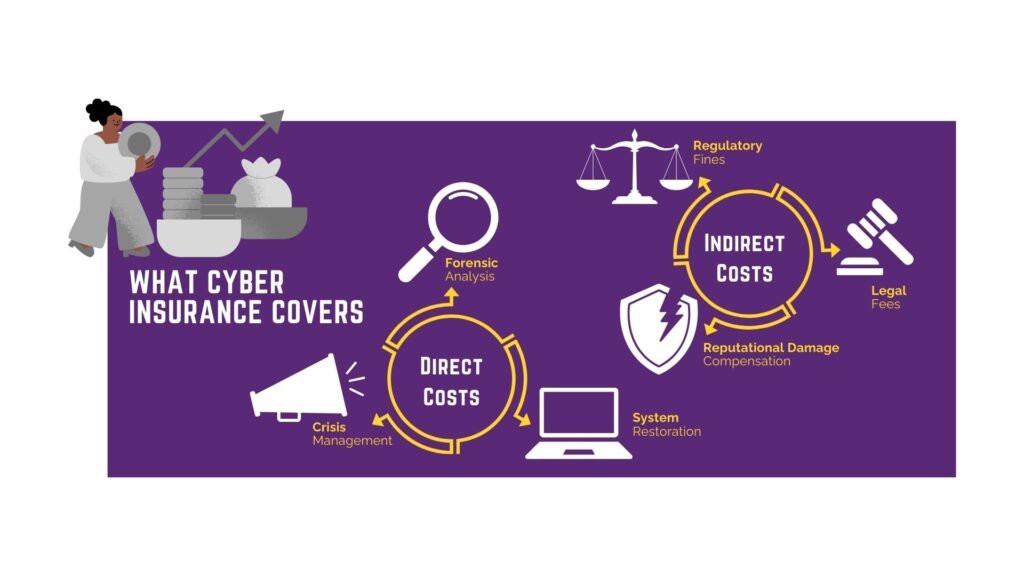

What’s Covered (Usually)

- Ransom Payments: But only if you prove “reasonable diligence” (spoiler: they decide what’s reasonable).

- Forensics Costs: Mandatory IR teams at $650/hour.

- Regulatory Fines: HIPAA/GDPR penalties (minus your $250k deductible).

- Business Interruption: Lost income during downtime (capped at 45 days).

What’s NOT Covered (The Fine Print Landmines)

- “Acts of War” Exclusions: When Russia attacked Ukraine, insurers denied claims for NotPetya damage. Why? “Cyber warfare.” One bakery lost $2M. The payout? $0.

- Negligence Penalties: Missed a patch? Default passwords? That’s “failure to maintain minimum security.” Denied.

- Reputational Harm: Patient records leaked? They’ll cover notification costs, but not fleeing customers.

The 3 Silent Claim-Killers

1. The Legacy System Loophole

A bank ran Windows Server 2008. Hackers exploited an unpatched flaw. Verdict: “Unsupported OS = negligence.” Claim rejected.

Fix: Document every end-of-life system. Provide compensating controls.

2. The Voluntary Payment Void

You pay a $200k ransom. Later discover the insurer had negotiators on standby. Claim denied.

Rule: Never engage hackers without insurer approval.

3. The Bodily Injury Black Hole

Hackers disabled a ventilator firmware update. The patient died. Insurer argued: “Physical harm isn’t digital loss.” A $15M lawsuit went uncovered.

Premium Nightmares: How Insurers Profit From Fear

After our breach, renewal terms arrived:

- 600% premium increase

- Mandatory $500k MDR service

- Exclusion for all supply-chain attacks

Worse, they demanded:

- Full network segmentation within 90 days

- Weekly phishing tests (95% pass rate)

- Air-gapped backups (verified monthly)

Translation: Do everything you should’ve done pre-breach or get dropped.

The Survival Playbook

Before Buying

- Demand Silent Cyber Clarity: Ensure policies cover non-specific cyber incidents (like power outages from ransomware).

- Test Sub-Limits: Crisis PR coverage often caps at $50k — a drop in your breach ocean.

- Verify IR Partners: Refuse forced “preferred” teams. Demand your own.

During Claims

- Assume Bad Faith: Record every call. Demand denial reasons in writing.

- Fight War Exclusions: Argue attribution to nation-states is impossible.

- Sue If Necessary: A manufacturing firm won $4.7M proving insurer negligence.

The Unspoken Truth

Cyber insurance isn’t a shield. It’s a bet against yourself. After our $5M ordeal:

- We spent $1.2M meeting new security demands.

- Premiums now cost more than our SIEM.

- We still bought it — because hospitals require it.

But we treat it like a grenade with the pin pulled.

“Cyber insurance is a tax for the unprepared. And we’re all unprepared.” — CISO who survived 3 claim battles

How Debit Cards Changed Banking Trust and What It Means for Financial Inclusion